As Alice Cooper put it in his classic 1972 song, Schools Out, “No more pencils, no more books, no more teacher’s dirty looks.” We can all recall the energetic vocals and guitar riff, but what about those ‘teachers dirty looks?’ It might be because the teachers, who are worn out by the school year, are just as eager for summer break as the students. With the average age of a Connecticut teacher being around 43 years old, many are likely dreaming of the time when they can enjoy an endless summer in retirement. School may be out, but if you read on, retirement class is in session. This is a great time to take a moment and review progress. It’s also time for me to give you my educators’ cheat sheet of the top 5 things to consider when planning for that retirement.

Great Guaranteed Retirement Income

The Connecticut Teachers Retirement System (CTRS) is a significant income benefit for retirement, with the average teacher payout at normal retirement age being roughly $58,000 in 2023. For those taking early retirement, that average dropped to roughly $50,000. When ranked nationally, it puts CT teachers as having the highest paid benefits in the country. Because Teachers in CT don’t pay into Social Security, their pension includes a mandatory cost of living adjustment (COLA), which means these benefits can continue to increase with inflation. This helps give the pension a ton of staying power and makes it a retirement cornerstone for most teachers.

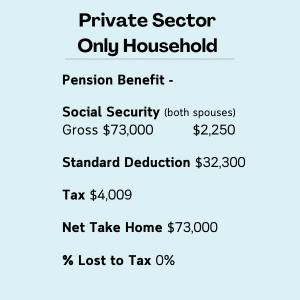

The Taxes

The downside to the pension is that unlike Social Security, it is fully taxed at the federal level. This means if we compare the taxation of two couples where one is a teacher and the other worked in the private sector, more of the guaranteed income for the teacher household will be taxed in retirement. I’ve provided a comparison of two 65-year-old couples with equivalent income in retirement. The household with the teacher pays more in taxes because their pension doesn’t get the same tac treatment as Social Security. (Teacher household $19,550 is counted towards taxes, Non-teacher household only $2,250). This means that down the road both Required Minimum Distributions (RMDs) and any potential ROTH conversion can become more expensive tax-wise. This is why we believe many teachers should consider ROTH options while working, to help provide greater tax control during retirement. There are many reasons why this can ensure more success and we encourage you to reach out for some analysis to see if this will help you with your specific situation.

Due to teachers having more consistent retirement income, distributions tend to be in larger chunks early on to supplement travel or giving to children or grandchildren. In these instances, ROTH distributions become much more tax efficient. Additionally, the death benefits of ROTH accounts to beneficiaries pass income tax-free as well, making it a great legacy option.

The Windfall Elimination Provision (WEP)

This is a tricky area, best served by example, as there is so much that goes into this calculation that typically we have to use software to figure it out using all of your earnings records from your Social Security statement. Suppose you are a teacher that had summer jobs where Social Security was withheld, or that you had other employment prior to becoming a teacher. This subjects you to the dreaded Windfall Elimination Provision (WEP). This means you will not get your whole calculated Social Security check because you didn’t pay in during all of your working years. For example, if you’re monthly benefit was $1,640 and your non-covered pension was $1,000, the max reduction in your Social Security benefit would be $500. So as stated earlier, average teachers’ pensions in CT are around $4,833 per month ($58,000 per year). The maximum WEP reduction is 50% of the non-covered pension amount (In this case could be as high as $2,416).

Purchasing Additional Retirement Credits

This is certainly an option for many teachers who have worked in other systems or just want to use a portion of their 403B funds to purchase more retirement credits. There are some factors to be aware of regarding the Connecticut Teachers Retirement System. First off, it is currently only 51% funded, which means it does not have all the funds currently required to pay out its promised pension obligations. In addition, about 70% of the unfunded liability is due to legacy debt that has already been incurred by the program. This means that increasing contributions or changes in payout options for future retirees might be on the table in the future. So, when purchasing additional credits, plan stability should be a major consideration. This is where a discussion with us at Route65 Financial about other guaranteed income options to avoid centralizing retirement income risk into only one program might be a prudent consideration.

Doing Some Analysis Early

Considering that retirement from teaching could last 30-plus years, we feel it is wise to evaluate your current situation and see if there are some adjustments that can be made to tailor your plan to your family and specific circumstances. In the example provided above, a $20,000 annual IRA distribution (figured to be about 4% of $500,000) will cost you another $2,400 in taxes. For the private sector household, that tax bill goes from zero to $423. Over a 30-year retirement that could be about $60,000 more in taxes, assuming that taxes don’t increase any time during your retirement. If this all seems complicated, please reach out. We can review your goals, sift through the numbers, do some analysis, and get you moving on a plan that makes sense. For once, allow us to do your homework for you, and get you ready for that one final time of “No More Pencils, No More Books!”