Roth IRAs are appealing due to their potential for tax-free income, but there are many misconceptions about them and the process of conversion. Before diving into those complexities, let’s review a few key Roth terms and concepts.

Contribution: A contribution occurs when funds are transferred from a bank account to a Roth IRA account. Annual contribution limits are $7,000 ($8,000 if you're 50 or older), and there are income limitations that may restrict your ability to contribute the maximum amount.

Transfer: A transfer is the movement of funds between two like accounts. For example, if funds move from one Roth IRA account to another, it’s considered a transfer.

Conversion: A conversion changes the tax status of funds from pre-tax to taxed by moving money from a Traditional IRA to a Roth IRA. It’s important to note that a conversion is not a contribution, and there’s no limit on the amount of funds that can be converted. However, taxes are due on the conversion amount, which could affect your tax situation:

- Taxable Income: The conversion amount is added to your taxable income for the year. For instance, if you earn $120,000 and convert $100,000, your taxable income for that year would be $220,000.

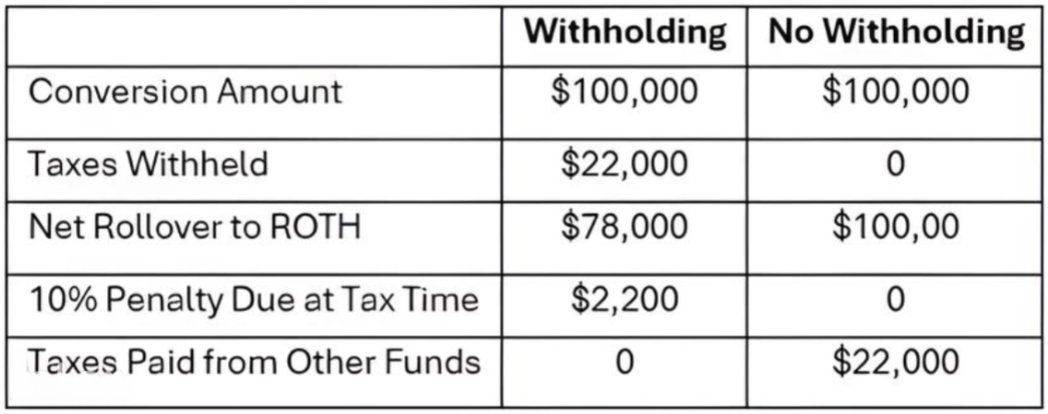

- Tax Withholding: You can choose to have taxes withheld during the conversion but be cautious. If you’re under 59 ½, withheld taxes count as a premature IRA distribution, subjecting them to a 10% penalty. For example, if you’re 47 and convert $100,000 with 22% tax withholding, it could result in penalties. It’s generally more cost-efficient to cover the taxes from funds outside your retirement accounts.

- Optimal Conversion Timing: The best time to convert is typically when your income is lower, such as when one spouse loses a job or retires earlier than the other. Lower income may allow you to convert more funds without pushing you into a higher tax bracket. Conversely, selling a business or investment property could increase your income and result in higher taxes on the conversion.

There are scenarios where converting with minimal tax impact is possible. Take James and Jill, both retired at age 66, with a combined Social Security income of $48,000 and $20,000 in annual IRA withdrawals. With a standard deduction of $32,000, their household income is $26,000, meaning no federal income tax is due. However, by converting an additional $10,000, they would incur a $1,223 tax bill—an effective tax rate of 12.23% on that conversion.

Advantages of This Strategy: Converting allows future access to potentially tax-free funds, locking in the current tax rate, and offering protection against possible future tax increases. Additionally, under the SECURE Act, non-spouse beneficiaries must withdraw inherited IRA funds within 10 years. For Roth IRAs, these distributions remain tax-free, unlike Traditional IRAs, where the distributions are taxable.

There are numerous strategies for Roth conversion planning, such as using non-retirement funds first, bunching charitable contributions into a Donor-Advised Fund, or utilizing Charitable Gift Annuities or Charitable Remainder Trusts for tax relief. If you’re interested in learning more, please reach out to discuss your options. We’re here to educate you on the possibilities.